Understand how franking credits impact your real dividend income with this franking credit calculator.

When you receive dividends from Australian shares, you’re often entitled to a franking credit, a tax credit attached to your dividend that represents the company tax already paid on those profits.

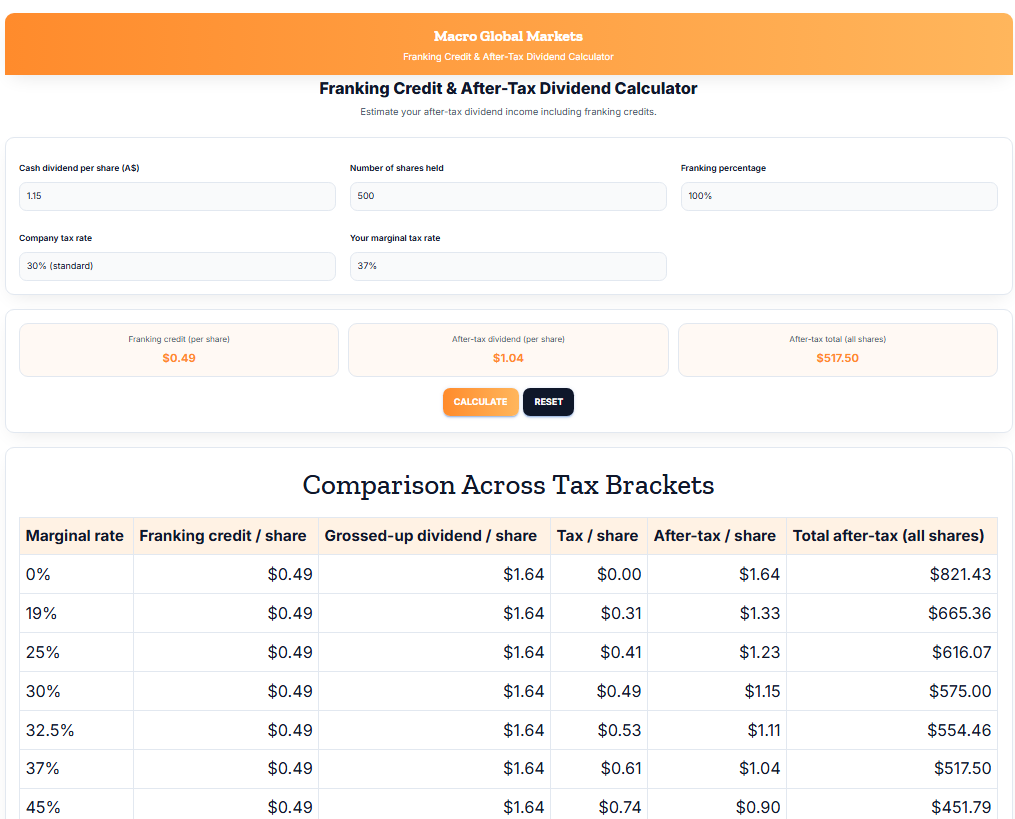

Use the calculator below to instantly see how franking credits and your marginal tax rate affect your after-tax dividend yield.

Macro Global Markets

Franking Credit & After-Tax Dividend Calculator

💡 Share or Embed This Calculator

Found this calculator helpful? Add it to your website or share it with your audience:

Tweet This • Share on LinkedIn • Share on Facebook

Tip: Embed this calculator on your blog, client portal, or newsletter to help readers calculate their after-tax dividend yield — and link back to Macro Global Markets for the official version.

How the Calculator Works

This calculator estimates your franking credit, gross-up amount, and final after-tax dividend.

It uses the standard Australian imputation formula:

Franking credit = Dividend × (Company tax rate / (1 − Company tax rate)) × Franking percentage

For example, if a company pays a 70 cent fully franked dividend and its corporate tax rate is 30%, the franking credit is:

0.70 × (0.30 / 0.70) = $0.30

Your grossed-up dividend equals $1.00, representing the full pre-tax profit distributed to shareholders.

The calculator then applies your marginal tax rate (including Medicare levy if relevant) to determine your after-tax income.

What Are Franking Credits?

Franking credits (also called imputation credits) were introduced to prevent double taxation of company profits.

Since companies already pay tax on their earnings before distributing dividends, investors receive a credit for that tax when they lodge their personal tax returns.

- Fully franked dividend: 100% of company tax has been paid (usually 30% or 25% for base-rate entities).

- Partly franked dividend: Only part of the dividend carries a franking credit.

- Unfranked dividend: No company tax credit attached, you pay tax on the entire amount at your marginal rate.

When you lodge your tax return, the Australian Taxation Office (ATO) treats the grossed-up dividend as income, then subtracts the franking credit from your tax payable.

If your personal tax rate is lower than the company’s rate, you may receive a refund of the excess franking credits.

If it’s higher, you pay the difference.

Example: How Franking Credits Affect Investors

| Investor type | Marginal tax rate | Dividend (cash) | Franking credit | After-tax income | Outcome |

|---|---|---|---|---|---|

| Retiree (0%) | 0% | $0.70 | $0.30 | $1.00 | Full refund of franking credit |

| Average earner | 32.5% | $0.70 | $0.30 | $0.67 | Pays ~3 cents tax overall |

| High-income earner | 47% | $0.70 | $0.30 | $0.53 | Pays ~17 cents additional tax |

Takeaway: The lower your marginal tax rate, the more valuable franking credits become.

Why After-Tax Yield Matters

Many investors compare shares on headline yield, the cash dividend divided by share price.

But that can be misleading. Two companies might both offer a 5 % yield, yet the after-tax result can vary by more than a full percentage point once franking credits and your tax bracket are considered.

Understanding your after-tax yield helps you:

- Compare Australian and global dividend stocks fairly

- Build a tax-efficient income portfolio

- Forecast real cash flow for SMSFs and retirees

- Decide whether to reinvest or withdraw dividends

Who Can Use Franking Credits

You may be eligible to claim franking credits if you are:

- An Australian resident for tax purposes

- The beneficial owner of the shares when the dividend is paid

- Satisfying the holding-period rule, generally holding the shares “at risk” for at least 45 days (90 days for preference shares)

- Not using the shares primarily for dividend-stripping or short-term tax benefits

Non-residents generally cannot claim franking credits but benefit from the fact that fully franked dividends are exempt from withholding tax.

SMSFs and Franking Credit Refunds

Self-Managed Super Funds (SMSFs) often benefit significantly from franking credits because:

- In accumulation phase, SMSFs pay only 15 % tax on earnings, below the 30 % company rate, so they usually receive a partial refund.

- In pension phase, SMSFs may pay 0 % tax, resulting in a full refund of franking credits.

That’s why franking credits remain a crucial consideration for retirees relying on dividend income.

Holding-Period Rule Explained

The holding-period rule ensures that franking credits go to genuine long-term investors, not short-term traders.

You must hold the shares at risk (not hedged) for at least 45 days (excluding purchase and sale days) between the ex-dividend date and the payment date.

If you sell too quickly, or use derivatives to protect against price movements, you may lose eligibility for the credit.

The calculator includes a toggle to reflect this rule, set “No” if you haven’t met it, and the franking credit will be removed from the result.

Company Tax Rates in Australia

Most large companies pay 30 %, but smaller base-rate entities (turnover under $50 million and <80 % passive income) pay 25 %.

This affects the size of the franking credit:

| Company tax rate | Franking % | Franking credit on $0.70 dividend |

|---|---|---|

| 30 % | 100 % | $0.30 |

| 25 % | 100 % | $0.23 |

| 30 % | 80 % | $0.24 |

Franking Credit Myths and Clarifications

- “Franking credits are a bonus.”

They’re not free money, they simply prevent double taxation on profits already taxed at the corporate level. - “You always get a refund.”

Only if your personal tax rate is below the company’s. Higher-income earners may owe additional tax. - “Franking credits don’t matter in super.”

They matter greatly, especially for SMSFs in pension phase. - “You lose franking credits when shares fall in price.”

Price movement doesn’t affect eligibility, but selling too soon may violate the holding-period rule.

How to Use the Calculator for Portfolio Planning

- Enter your expected dividend per share.

- Select the franking percentage (check the company’s latest dividend announcement).

- Choose the company tax rate (25 % or 30 %).

- Select your marginal tax rate, if unsure, use your last tax bracket.

- Toggle your residency and holding-period rule status.

- Click Calculate to see:

- Franking credit value

- Grossed-up dividend

- After-tax income per share

- Comparison table across tax brackets

This helps you compare investments and understand the true income value of franked dividends.

Common Dividend Imputation Questions

Can franking credits create a tax refund?

Yes. If your franking credits exceed your total tax payable, the excess is refunded by the ATO.

Can I claim franking credits through my broker or CHESS statement?

No. Your broker records dividends, but franking credits are claimed when you lodge your individual tax return.

What if I invest through an ETF?

The ETF passes through any franking credits it receives, which appear in your annual tax statement.

Do non-residents pay withholding tax on franked dividends?

Fully franked dividends are exempt from withholding tax, but unfranked portions may attract it.

Where can I verify the company’s franking percentage?

Check ASX announcements, the company’s dividend declaration, or your broker’s tax summary.